Long story short:

- The Netherlands' ERE scheme (live since January 2026) turns every public-charger kWh into a tradable CO₂ credit worth €0.06–0.18 per kWh (example estimation).

- Chargers need an integrated MID meter by January 1, 2027. The real winners will be operators whose software stack feeds clean data into the NEa register.

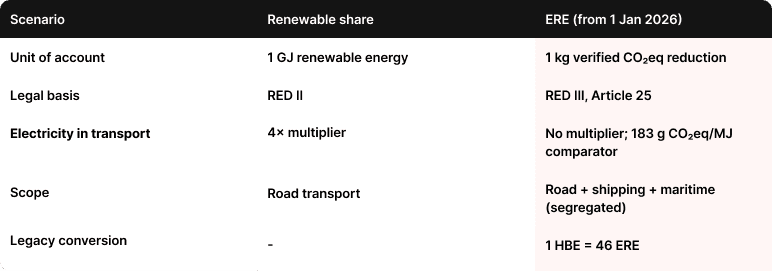

From 1 January 2026, every kWh delivered into an electric vehicle at a Dutch public charger mints a new revenue stream. Not through the tariff. Through a tradable emission credit worth 1 kilogram of verified CO₂ reduction. The ERE (Emission Reduction Unit) system has replaced HBE and wired EV charging economics into fuel-supplier obligations. The spreadsheet just changed.

For CPOs, aggregators, and fleet operators, the implications run deeper than compliance. A charging session in the Netherlands now carries two revenue streams – energy sold and a compliance credit that can be traded. Margin models need to be rebuilt around that, and so does the reporting stack. Accurate metering and verifiable session data stop being a back-office concern.

What is ERE and what it replaced

The Netherlands implemented the Brandstoftransitieverplichting as its transposition of RED III (Directive 2023/2413). Article 25. The register is run by the Netherlands Emissions Authority (NEa).

The obligation ramps from 14.4% GHG-intensity reduction in 2026 to 27.1% by 2030, split into three non-fungible credit codes: LRE (road), BRE (inland shipping), ZRE (maritime). The electricity comparator is 183 g CO₂eq/MJ, against 94 g CO₂eq/MJ for general fuel – which is why removing the 4× multiplier didn't gut the EV case.

What ERE adds per kWh

Dutch public fast chargers have lived with low utilization for years. ERE doesn't fix that, but at April 2026 prices and the 2026 national renewable share of 50.5% (derived from 2024 CBS data with a two-year lag):

A typical ultra-fast site with decent throughput lands a five- to low-six-figure annual ERE line. System-wide effects are modeled in CE Delft's March 2025 analysis.

MID meters and the 1 January 2027 deadline

Every booking must originate from a charger with a MID-certified meter built into the unit itself. However, external meters in the distribution cabinet can be problematic. A February 2026 survey showed that 52% of kilometers driven in the Netherlands come from private (home) electric vehicle chargers.

However, meters from older models, such as the Easee Charge, EV Box Elvi, Wallbox Pulsar, Tesla Wall Connector Gen. 2, and go-e Gemini, are on the swap list. Exchanges cost €800–1,500 per point.

That's only the physical layer. The second, often underrated, is software.

Where CPMS, OCPP and OCPI decide ERE outcomes

ERE settles event by event. A session has to travel from the charger into the NEa register through a validated data chain, with energy metrics, timestamps, and renewable-origin proof where the 100% rate is claimed. A CPO's CPMS has to:

- aggregate and normalize data from heterogeneous chargers (multiple vendors, multiple OCPP versions)

- expose that data through OCPI to roaming and settlement counterparties

- carry an integration layer for inboekdienstverleners, the brokers that book EREs into the register

Operators who bought a SaaS CPMS a few years back are finding the vendor has no ERE roadmap, or that the custom-build quote is prohibitive. Platform migration to a solution with full control over data, in a licensed or bespoke model, is becoming a live procurement topic.

The bigger the network, the louder the economics argue for system ownership and source access.

Dynamic pricing is the adjacent angle. ERE income lets operators subsidize off-peak tariffs without destroying margin – but that needs a tariff engine wired to network data and an ERE calculator running close to real time. Not an out-of-the-box feature.

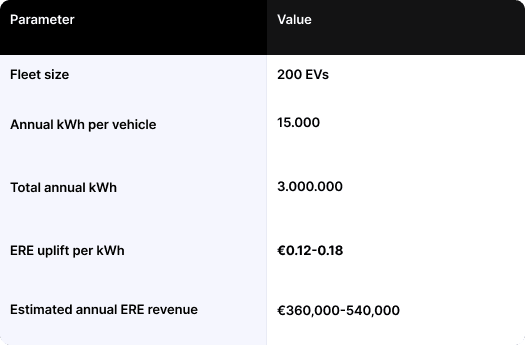

Depot-charged EV fleets. The strongest B2B case

Biggest single wins go to fleets with their own depot charging and onsite PV documented at the same WOZ-registered address. Worked example, 100% verified renewable:

That's not a subsidy. It's the market price of a tradable right. For fleet operators, backend software (CPMS, settlement, emissions reporting) stops being a maintenance cost and starts landing directly on the P&L.

Brokers and the software pressure

60+ brokers are registered with NEa; 40–50 are operationally active, with commissions between 15% and 27.5%. Under the hood it's a data business: telematics ingest, NEa rule validation, batch booking, settlement. A broker without solid automation won't hold margin.

For investors, there are two vectors:

- consolidation among brokers through 2026–2027 (M&A looks near-certain)

- valuation premium for CPOs with compliant hardware and a mature CPMS

The pressure on EV software vendors is running hotter than on charger manufacturers.

ERE vs the wider European market

Germany's THG-Quote and the French, Spanish and Italian transpositions of RED III each carry their own flavor. A single European carbon-credit market for transport doesn't exist and won't for several years. Cross-border fleets and networks have to plan for country-by-country compliance, not one API for everything.

That's regulatory risk – and an opportunity for anyone building a software layer ready to port to the next market. The Netherlands is first. Not last.

The takeaway

ERE is live and already rewriting the investment math. Most of the value won't go to the operator with the best hardware or the cheapest energy. It will go to the ones that control their own network data, integrate it into the NEa register without friction, and read the ERE price signal in hours rather than months. It's a test of digital infrastructure, not of steel in the ground.

The bottleneck is no longer the charger (alone).

It's the layer between the charger and the register. Session data has to be clean enough to report and fast enough to react when the price moves. CPOs running on a closed CPMS are now discovering they don't actually own the data their business depends on.

Solidstudio develops CPMS platforms that operators actually own. The data schema, regulator integrations, settlement logic – the operator controls all of it. No vendor lock-in on what gets reported, or when.

----------------

FAQ

Is the scheme actually in force, or still being debated?

In force. The Brandstoftransitieverplichting took effect on 1 January 2026 and the Eerste Kamer formally adopted the implementing legislation on 31 March 2026 with retroactive application.

Can businesses outside the Netherlands participate?

Only Dutch-registered operators with Dutch charging infrastructure and a Dutch grid connection can book EREs. Foreign-owned businesses operating Dutch subsidiaries can participate through those subsidiaries.

What happens to unused HBE credits?

They convert automatically after the 2025 compliance year closes on 1 May 2026, at a rate of 1 HBE = 46 ERE, preserving category labels (advanced, Annex IX-B, conventional). No HBEs convert to ERE-E – new ERE-E can only be created from 2026-forward bookings.

Are ERE prices public?

No. The market is bilateral and OTC. Brokers publish indicative ranges (roughly €0.30–€0.47 per ERE in early 2026). From May 2026 onwards, the NEa will publish volume reports six times per year.

Is the ERE income from home charging taxable?

Tax treatment for private users is unclear pending Belastingdienst guidance. Businesses should treat it as ordinary revenue.

How do I know if my charger has a MID meter?

Check the product datasheet for MID-certified or EN 50470 compliant. When in doubt, ask the manufacturer directly – installation-era documentation is the most reliable source.

When can solar panels increase my ERE yield?

Only for businesses, and only with a separate certified production meter (brutoproductiemeter) installed on the PV system, co-located with the charger on the same WOZ-registered property. For private users, solar panels have no effect on the ERE calculation.

What happens after 1 January 2027?

External MID meters become non-compliant. Only chargers with integrated MID-certified meters (or a dedicated separate grid connection) can continue booking EREs. Expect hardware churn through 2026.

Is this something other EU member states will copy?

Some variation already exists (Germany's THG-Quote). Full harmonization isn't on the short-term EU agenda, but the ERE model is the most consumer-accessible implementation of RED III so far and is being studied by other national regulators.

-----------------

Sources

- RED III (Directive 2023/2413):

https://eur-lex.europa.eu/eli/dir/2023/2413/oj - Renewable Transportation Fuel Policies:

https://dieselnet.com/standards/eu/fuel_renewable.php - Energieverbruik uit hernieuwbare bronnen stijgt naar 20 procent:

https://www.cbs.nl/nl-nl/nieuws/2025/23/energieverbruik-uit-hernieuwbare-bronnen-stijgt-naar-20-procent - CE Delft's March 2025 analysis:

https://cedelft.eu/wp-content/uploads/sites/2/2025/04/CE_Delft_240338_Prijseffecten_ERE-systematiek_Def.pdf - Netherlands Emissions Authority (NEa)

https://www.emissionsauthority.nl/topics/renewable-energy-for-transport - Verbruik van hernieuwbare energie, 1990-2024 https://www.clo.nl/indicatoren/nl038541-verbruik-van-hernieuwbare-energie-1990-2024

- Lijst van inboekdienstverleners

https://www.emissieautoriteit.nl/documenten/2026/02/02/lijst-van-inboekdienstverleners - Solidstudio.io https://solidstudio.io