Long story short:

Covid made opting out of digital tools uneconomic. Adoption timelines collapsed from years to months. The oil shock is now doing the same to liquid fuel, and charging software (not vehicles or batteries) is the next constraint.

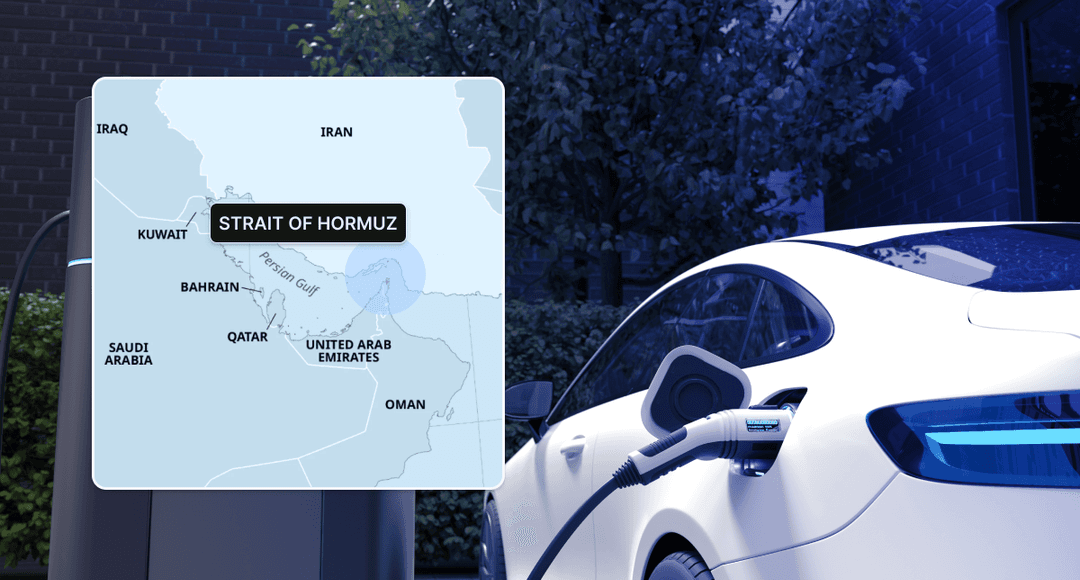

Airlines hedge their jet fuel. It's the first thing you learn about the industry. The second is that hedges work against noise, not against tankers refusing to leave the Gulf. CNN reported as much this week. Five years out, shocks like these tend to leave fingerprints all over an economy.

Five years ago, Covid didn't invent remote work, telemedicine, or e-commerce. It just made opting out impossible. Something similar is now happening to liquid fuel, and aviation is where the alarms went off first.

What Covid actually did

The Zoom call existed before 2020. So did Shopify, Peloton, DoorDash, electronic signatures, and telehealth. What the pandemic changed was the cost of refusing them. A GP who had avoided video consultations for a decade did one on Tuesday. Cloud ERP contracts that had sat unsigned on manufacturers' desks for years went through by Friday.

McKinsey, surveying executives mid-pandemic, found that companies had compressed three to four years of digital adoption in customer interactions, supply chains, and internal operations into a matter of months. Digital product roadmaps moved forward by closer to seven.

Forcing functions doesn't invent technology. They shorten the runway. The tech is usually waiting already, the economics are usually close enough, and the only thing missing is a reason to stop deferring the decision. Then somebody cuts off the oil.

Why jet fuel is the trigger, not the story

Airlines show up first because they sit at the end of the most exposed supply chain in the global economy. IATA puts jet fuel at close to 30% of the industry's operating expenses. There's no substitute you can drop into a 737 tomorrow. When Brent moves, earnings move with it.

And when a shooting war threatens the Strait of Hormuz, the move isn't gentle. Twenty million barrels of oil a day pass through that chokepoint, about a fifth of global petroleum consumption, per the U.S. EIA.

But airlines are just where it gets loud first. Road freight, maritime shipping, commercial fleets, municipal buses, last-mile delivery. Every sector on that list runs on refined hydrocarbons. The arithmetic the airlines just worked through applies to all of them.

A cost line that used to be merely volatile becomes one that's also strategically indefensible. The conversation changes. Procurement stops asking whether to electrify. The question becomes how fast.

Practically, that shifts capex. Money pencilled in for the 2030s quietly slides into this decade's budgets. Companies that were hedging politically against the transition stop mentioning that they ever were.

What actually gets built next

Not electric long-haul planes. That timeline hasn't changed. Short-haul electric and hybrid aviation, sustainable aviation fuels, hydrogen for specific routes. These are decade-long bets with physics to solve.

The ground transport side is different. It's already further along, and it moves first. Battery-electric cars reached 17.4% of new EU registrations in 2025. Norway sits at 95.9%, which is basically the whole market.

China, meanwhile, has spent more than a decade building its EV industry as a national project and is now exporting the results. The IEA counts 12.4 million electric cars produced there in 2024, over 70% of global output.

Commercial fleets, the part of the market that cares about total cost of ownership and not the showroom experience, have been running these numbers for years. At today's price, diesel barely wins. On the forward curves, it's already lost.

The trucks are coming too. Slower than the cars, faster than the sceptics think. IEA figures put electric medium- and heavy-duty truck sales past 90,000 globally in 2024, up nearly 80% year on year.

The bottleneck is no longer the vehicle

The cars are built. Batteries are rolling off the line in volume. The component supply chains are scaling, messily and loudly but scaling. The constraint has moved somewhere else.

Europe's public charging network grew by more than 35% in 2024, crossing one million points, according to the IEA. That sounds like progress, and it is. Hardware in the ground is a different thing from a charging session that actually completes.

Ask anyone running a charging network today what keeps them up at night. Almost never hardware. It's what sits behind the plug: OCPP-compliant backends. eMSP apps that don't crash at peak. Roaming protocols so a driver in Warsaw can charge in Lisbon without a second account.

Dynamic load balancing so a depot doesn't trip its own grid connection. Billing reconciliation across twenty payment providers. Authentication that actually works at minus ten degrees.

The Open Charge Alliance exists precisely to make all of this interoperable and unremarkable. It isn't there yet. JD Power's 2025 survey found that 14% of EV owners had shown up at a public charger and left without successfully charging. Nobody takes pictures of that layer. It's also where most of the things that go wrong, go wrong.

Building it is specialist work. That's the bet we've made at Solidstudio, working on exactly this layer for charge point operators and mobility service providers across Europe. The people actually doing this for a living stopped debating the transition a couple of years ago.

Timing is now the argument. Specifically, whether the software stack will be ready when the volume arrives.

The part that gets missed

Energy transitions don't happen on enthusiasm. Price makes them happen, specifically the moment the alternative becomes more expensive than the switch. Covid was that moment for digital. The oil shock is playing out the same mechanic in slower motion, across everything that currently burns.

Adoption is no longer the open question. The volume is coming. Whether the charging network and the software behind it can keep up is.

- - - - - -

FAQ

Why are airlines hit first by oil shocks?

IATA puts jet fuel at close to 30% of airline operating expenses. That's structurally higher than for most other industries. Aviation has no short-term substitute either: you can't drop a new fuel into a 737 tomorrow. When Brent moves, airline earnings move with it, which is why aviation is usually where oil shocks surface in the financial press before anywhere else does.

How much oil passes through the Strait of Hormuz?

About 20 million barrels per day in 2024, according to the U.S. EIA. That's about a fifth of global petroleum liquids consumption moving through a single chokepoint. The concentration is why geopolitical risk in the Gulf moves prices so quickly. The route carries both crude and refined products bound for Asia, Europe, and North America, with no easy alternative.

What's the real bottleneck for EV adoption today?

Increasingly, it's the software layer behind public charging, not vehicles or batteries. The IEA reports Europe's public charging network crossed one million points in 2024, a 35% year-on-year jump. JD Power's 2025 survey still found that 14% of EV owners had visited a charger and left without successfully charging. That gap is where protocols like OCPP, backend reliability, roaming, and load management live.

How is the oil shock like Covid for digital adoption?

Both function as forcing events rather than invention events. Covid didn't create Zoom, telehealth, or cloud ERP. It just made opting out of them uneconomic. McKinsey found adoption timelines compressed by three to four years in months. Oil volatility does the same thing to electrification. It doesn't invent EVs or chargers; it removes the option of deferring them.

Where does electric truck adoption actually stand?

Electric medium- and heavy-duty truck sales exceeded 90,000 globally in 2024, per the IEA, up nearly 80% year on year. The segment trails passenger vehicles but is on a steep curve. Total cost of ownership for fleets keeps narrowing the gap with diesel, and volatile fuel prices accelerate the math. Expect the pace to pick up, not slow down.

What is OCPP and why does it matter?

OCPP (Open Charge Point Protocol), maintained by the Open Charge Alliance, is the open standard that lets charging stations communicate with backend management systems. Together with OCPI (for roaming between networks), it's what makes public charging work across operators and borders. When drivers can't charge in another country or on another network, OCPP/OCPI implementations are usually where the failure sits.